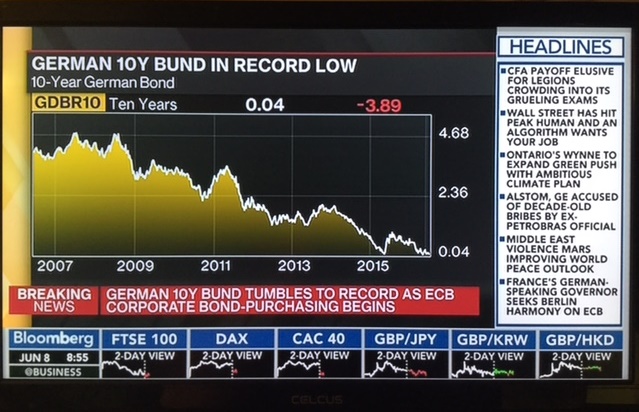

An historic moment in world finance came to pass this morning. Today, the European Central Bank (ECB) starts to buy Eurozone corporate bonds. French banks on behalf of the ECB kicked off the debt purchasing programme by buying the bonds of a French utility company as the European markets opened. The result is that in order to get any decent return on their investments, funds (such as the pension funds which invest the savings of tens of millions of people across the continent) are crowded out from securing these instruments at a reasonable return. What’s more as can be seen in this screenshot the return on government debt is now at all-time lows, so again savers worldwide are set to suffer.

The knock on effects of this unprecedented action are hard to calculate – and surely this is the key point? Yet again we see the desperation and determination of the world’s central bankers and monetary policy elite to do ‘anything it takes’ to stop the necessary Great Correction from talking place after the 2008/9 financial crisis. What is clear is what they are doing is likely to have unintended consequences that make matters worse. Will private funds have to trade down to the junk bond market to get returns? If so these rates are likely to fall and so may not reflect their true risk.

While saving us from pain now, the actions of the BOE, ECB and the FED are ensuring that correction in the markets of many asset classes will be bigger and more damaging for ordinary working people across the EU. It will be interesting to see just what the ECB thinks constitutes ‘quality paper’ under this scheme. For example, can we expect the ECB to buy bonds in Italian, Spanish and Greek companies? Somehow I think not. So what signal does this send to investors about the future value of these businesses in periphery Eurozone countries? Yet another unintended consequence…

The knock on effects of this unprecedented action are hard to calculate – and surely this is the key point? Yet again we see the desperation and determination of the world’s central bankers and monetary policy elite to do ‘anything it takes’ to stop the necessary Great Correction from talking place after the 2008/9 financial crisis. What is clear is what they are doing is likely to have unintended consequences that make matters worse. Will private funds have to trade down to the junk bond market to get returns? If so these rates are likely to fall and so may not reflect their true risk.

While saving us from pain now, the actions of the BOE, ECB and the FED are ensuring that correction in the markets of many asset classes will be bigger and more damaging for ordinary working people across the EU. It will be interesting to see just what the ECB thinks constitutes ‘quality paper’ under this scheme. For example, can we expect the ECB to buy bonds in Italian, Spanish and Greek companies? Somehow I think not. So what signal does this send to investors about the future value of these businesses in periphery Eurozone countries? Yet another unintended consequence…